As of March 30, 2026, 05:30 AM UTC, 49 tokens are scheduled to unlock a combined $472.98 million in vested supply, based on current prices and reported market caps. The table includes each token’s price, reported market cap, percentage of maximum supply already released, and the notional value of the upcoming unlock.

Large‑cap names HYPE, SUI, ENA, EIGEN, and OP dominate the notional flow, while a long tail of DeFi, infra, gaming, and micro‑cap tokens introduces localized volatility and niche opportunities for event‑driven traders. Several projects still sit below 30% released supply, reinforcing a key 2026 theme: tokenomics and vesting schedules remain central to the risk–reward profile of early‑stage assets.

Top unlocks by value

| Token | Price ($) (Mar 30, 05:30 UTC) | Upcoming Unlock Value | Reported Market Cap | Released % of Max Supply |

| HYPE | 37.90 | $375.84M | $9.01B | 41.53% |

| SUI | 0.847 | $38.43M | $3.30B | 39.04% |

| ENA | 0.09 | $19.06M | $761.60M | 52.24% |

| EIGEN | 0.167 | $6.16M | $108.19M | 29.18% |

| GUN | 0.016 | $6.87M | $25.79M | 16.47% |

| OPN | 0.201 | $6.44M | $28.39M | 23.06% |

| OP | 0.102 | $3.19M | $215.80M | 46.97% |

| KMNO | 0.017 | $3.89M | $72.31M | 67.92% |

| ZETA | 0.047 | $2.13M | $61.95M | 62.56% |

| REZ | 0.003294 | $1.40M | $25.70M | 69.65% |

HYPE carries the single largest notional unlock at $375.84 million on a $9.01 billion market cap, with 41.53% of max supply already circulating. This is a mid‑stage supply profile where unlocks can still materially shift float and trigger hedging from funds, team wallets, and early liquidity providers.

SUI follows with a $38.43 million unlock versus a $3.30 billion market cap and 39.04% released, keeping dilution structurally relevant for one of the cycle’s flagship L1s.

ENA adds $19.06 million of supply on a $761.60 million cap and 52.24% released, a mid‑to‑late‑stage profile where unlocks remain meaningful but are more likely to be absorbed if liquidity holds.

EIGEN unlocks $6.16 million against a $108.19 million cap with just 29.18% released, placing it firmly in the early‑stage bucket where vesting remains a core part of the investment thesis.

GUN is structurally fragile: a $6.87 million unlock on only $25.79 million market cap with 16.47% of supply released suggests heavy marginal float hitting a relatively small base.

Late‑stage vesting (lower structural overhang)

- TET – 98.95% released, $27.05K unlock on a $2.54M cap.

- DCK – 93.94% released, under $1K unlock on a $131K cap.

- GTAI – 90.54% released, $1.81K unlock on a sub‑$1M cap.

- BMEX – 90.28% released, $296.48K unlock on a $9.46M cap.

- SVL, SKL – 86.46% and 87.29% released respectively, with modest unlocks relative to float.

Here, most dilution has already occurred; these events look more like incremental emissions than cliff unlocks.

Early‑stage vesting (higher structural risk over time)

- MMT – Only 5.13% released, yet a $518.67K unlock on a $21.48M cap.

- AA – 5.41% released, small absolute unlock but very early in the curve.

- ACS – 10.13% released, $46.03K unlocking on a $7.92M cap.

- CYPR – 10.00% released, $11.89K unlock on a $1.02M cap.

- GUN, OPN, ATH, NYAN – 16–26% released with visible unlocks, keeping vesting front‑and‑center.

For these tokens, vesting schedules will remain a key driver into 2027, and unlock weeks can be meaningful catalysts in either direction.

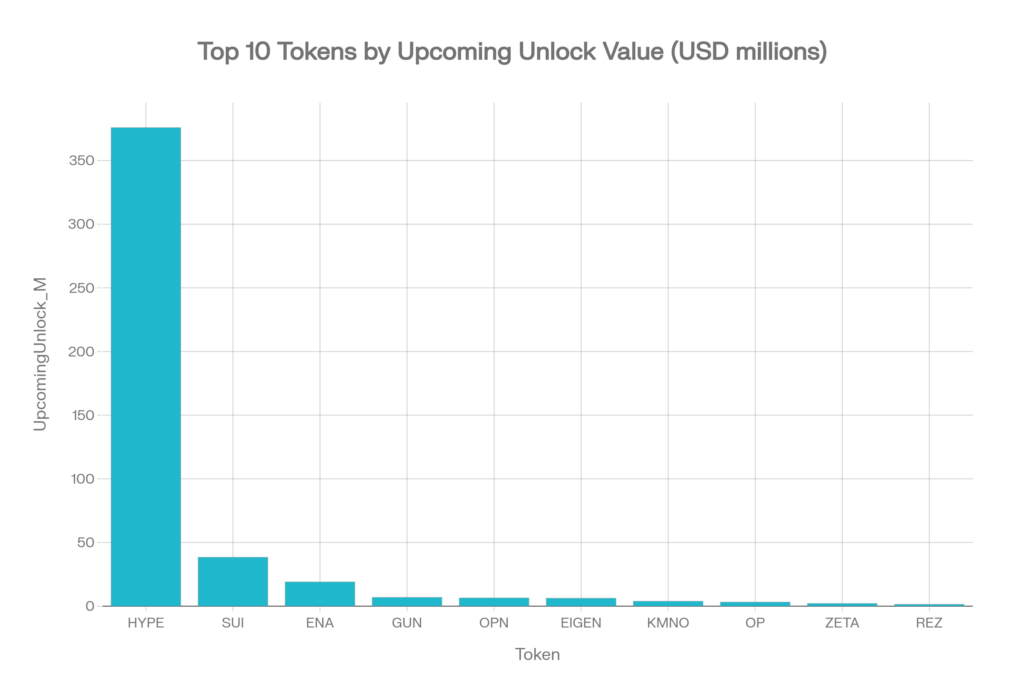

Market‑cap vs unlock size

A bar chart of the top 10 tokens by upcoming unlock value shows HYPE and SUI as clear outliers, followed by a second tier made up of ENA, EIGEN, GUN, OPN, OP, KMNO, ZETA, and REZ. HYPE’s bar towers over the rest, visually underscoring the sheer size of its scheduled release relative to all other names in this batch.

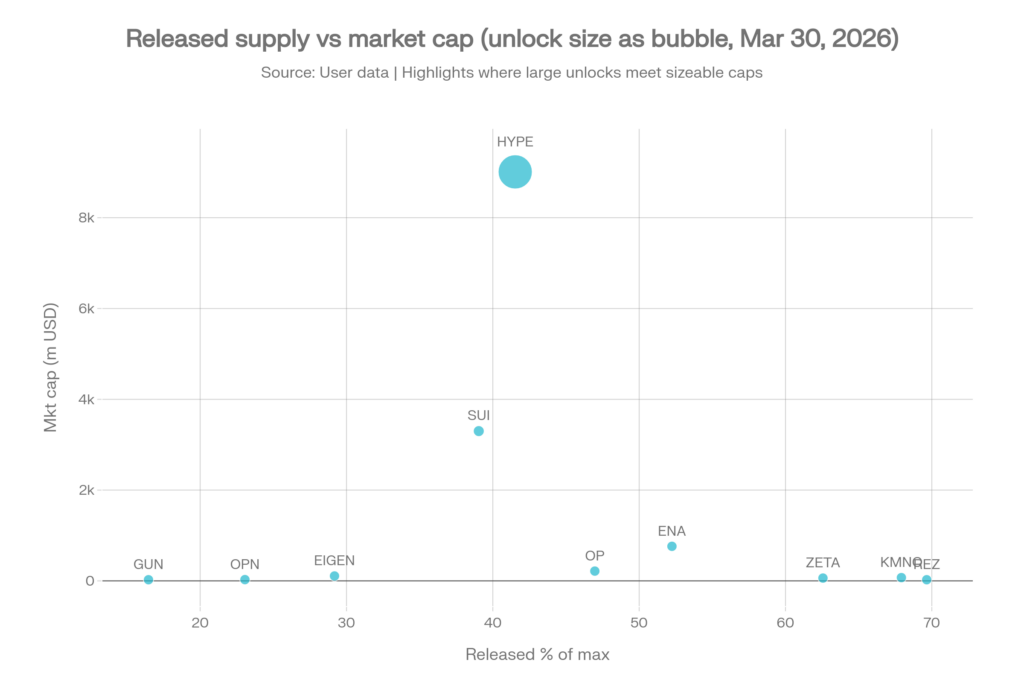

A bubble scatter plot maps released supply percentage (x‑axis) against reported market cap (y‑axis), with bubble size representing upcoming unlock value in USD millions. Large‑cap bubbles like HYPE, SUI, ENA, IOTA, OP, and AERO cluster in the upper‑middle of the chart, while early‑stage names with lower released percentages but chunky unlocks (for example, EIGEN, GUN, OPN) stand out toward the left.

- Large‑cap, large unlock: HYPE, SUI, ENA sit in the top‑right region of impact, combining deep liquidity with substantial new supply.

- Mid‑cap, chunky unlock: EIGEN, GUN, OPN, KMNO, ZETA form a cluster where unlocks are material relative to size and can amplify volatility when order books are thin.

- Micro‑cap, small unlock: Names like NYAN, AA, DCK, GTAI show low on both axes; absolute dollars are tiny but can still move illiquid books and attract high‑beta traders.

This visualization helps identify which unlocks are likely to be absorbed and which may temporarily overwhelm local liquidity.

Detailed Token Highlights

DeFi, liquidity, and infra‑adjacent names

Several DeFi, infra, and tooling‑style tokens in this batch have unlocks that can reshape governance and emissions:

- OP – $3.19M unlock on a $215.80M cap with 46.97% released, a mid‑cycle L2 governance asset where unlocks remain tradable but generally manageable.

- MANTA – $305.96K unlocking on a $27.96M cap with 60.42% released, consistent with a maturing tokenomics curve.

- AERO – $1.19M unlock on a $292.63M cap, 61.58% released, aligning with the broader DeFi liquidity infrastructure narrative.

- CETUS, CXT, ACS – Smaller‑cap liquidity and infra plays with 10–65% released and five‑ to six‑figure unlocks, where order‑book depth will matter more than headline size.

For these projects, unlocks can shift governance power, liquidity incentives, and yield dynamics across associated pools and protocols.

L1, L2, and core infrastructure

Tokens tied to base‑layer or infra themes include SUI, CELO, IOTA, AURORA, OP, ZETA, AERO, W, NAVX and others.

- SUI – Flagship L1 with a $38.43M unlock and only 39.04% of supply released, underscoring ongoing dilution risk that investors must price alongside ecosystem growth.

- IOTA – $662.06K unlock on a $232.15M cap with 83.82% released, indicative of a late‑stage emission profile where vesting is no longer the primary driver.

- AURORA – $143.41K unlock on an $18.62M cap, 50.63% released, sitting in the mid‑range of its lifecycle.

- ZETA, W, NAVX – Between roughly 53–63% released, with five‑ or six‑figure unlocks that can still drive idiosyncratic moves around event dates.

These names typically have deeper liquidity and derivatives markets, which can help absorb supply but do not eliminate the impact of concentrated selling.

Gaming, NFTs, and metaverse‑style names

While the sheet does not explicitly label sectors, several tickers such as FLOCK, SIDUS, HONEY, DICE, NYAN, GFAL likely align with gaming, NFT, or metaverse‑adjacent narratives.

- FLOCK – $897.67K unlock on a $16.71M cap with 33.52% released, a structurally meaningful event for a mid‑cap game‑adjacent token.

- SIDUS – $12.44K unlock with 77.08% released, more consistent with late‑cycle emissions.

- HONEY – $71.20K unlock on an $11.77M cap with 72.59% released, suggesting much of the structural overhang is already priced in.

- DICE, NYAN – Micro‑caps with tiny unlocks but very low prices, where even modest selling can move spot significantly.

For these tokens, unlock impact often depends as much on concurrent in‑game or ecosystem catalysts as on pure supply math.

Micro‑caps and tail risk

At the extreme tail, tokens such as NYAN, AA, DCK, GTAI, HMX, ATH exhibit small dollar unlocks but fragile liquidity profiles.

- NYAN – Unlock under $1K on a $73K cap with 25.61% released, a textbook thin‑liquidity, high‑beta profile.

- AA – 5.41% released, sub‑$2K unlock on a $59K cap.

- DCK – 93.94% released, sub‑$1K unlock, structurally late stage but still highly sensitive to order‑flow imbalances.

- GTAI, HMX, ATH – Similar micro‑cap setups with small unlocks that can still cause double‑digit intraday moves.

These tokens are unlikely to move the broader market but are magnets for volatility and slippage, making them attractive yet risky event‑driven trades.

Market Implications

Token unlocks introduce incremental sell‑side pressure, especially where allocations belong to early investors, teams, or ecosystem treasuries seeking liquidity. In prior cycles, large unlocks for headline names have triggered short‑term drawdowns when supply hit the market faster than new demand could absorb it.

For this batch:

- HYPE, SUI, ENA, EIGEN, OP form the core macro watchlist, given their size, liquidity, and narrative relevance across L1/L2 and infra ecosystems.

- Mid‑caps like GUN, OPN, KMNO, ZETA, MMT, MANTA, AERO may see outsized volatility relative to their market cap, especially where unlocks exceed typical daily volumes.

- Late‑stage names such as TET, DCK, GTAI, BMEX, SVL, SKL are less about structural overhang and more about whether fundamentals justify valuations now that most of the float is already live.

The scatter view of market cap versus unlock size highlights that several of the biggest dollar events occur in projects with enough depth to theoretically absorb them, but positioning and sentiment will ultimately dictate whether unlocks become buy‑the‑dip opportunities or exit liquidity.

Conclusion

This week’s $472.98M unlock across 49 tokens, highlighted in the latest tokenomics vesting updates, underscores how central token supply mechanics remain to the crypto market structure in 2026. While large‑cap events for HYPE, SUI, ENA, EIGEN, and OP dominate the headline numbers, the real opportunities and risks sit in the mid‑cap and micro‑cap ranges where unlocks interact with thin liquidity and uneven fundamentals.

{kind=link}