Between March 23 – 29, 2026, 50 tokens are scheduled to unlock fresh vested supply, spanning large-cap infrastructure, DeFi, AI, gaming, and micro-cap experiments. For each token price as of March 23, 06:00 AM UTC, reported market cap, percentage of maximum supply already released, and the upcoming unlock value for this week.

The projects are set to release approximately 76.36 million token, with an average float maturity of around 53.27% and a median of 50.71% of max supply already circulating. Large-cap names H, JUP, XPL, PARTI, and SOSO anchor the headline unlocks, while a long tail of DeFi, AI, and gaming tokens contributes localized volatility and niche event-driven opportunities.

Key Highlights

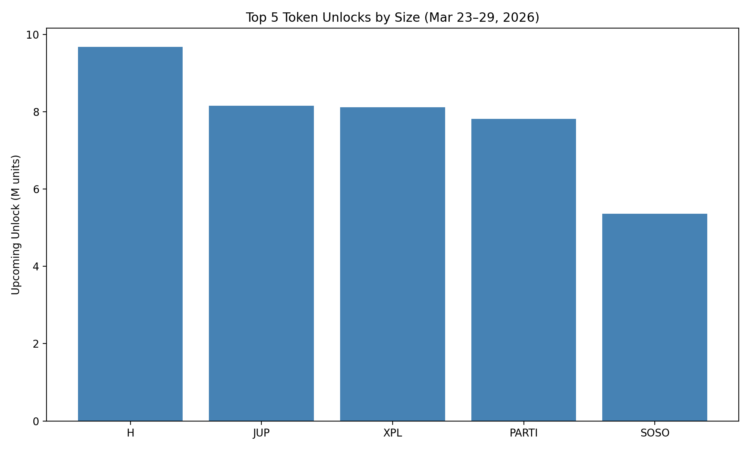

Top unlocks by value

The top 5 tokens by upcoming unlock size for March 23–29, 2026 are:

- H carries one of the week’s largest unlocks at approximately 9.68M on a reported market cap of 167.93M USD, with 25.16% of max supply already circulating. This mid-stage profile means each unlock still meaningfully shifts float and can catalyze hedging or de-risking from early stakeholders if liquidity thins.

- JUP unlocks around 8.15M against a 533.45M USD market cap and 51.13% released, placing it among the most closely watched events for traders active in high-liquidity majors.

- XPL’s 8.11M-unit unlock lands on a 204.68M USD capitalization with only 22.32% of supply live, highlighting an early vesting curve where each event adds significant marginal float.

- PARTI features a ~7.81M-unit unlock at a market cap near 20.43M USD and 44.97% released, implying a chunky event relative to project size and a still-developing float.

- SOSO rounds out the top group with 5.36M unlocking on a 125.43M USD cap and 29.29% released, a configuration that can amplify volatility if unlock recipients choose to sell into thin books.

High and low supply impact

The Released Percentage shows how far each token is through its vesting lifecycle. This lets us separate late-stage profiles from early-stage names where tokenomics remain the primary driver of risk–reward. Insights from Tokenomist further reinforce how vesting progress influences market behavior during unlock weeks.

Late-stage vesting (lower structural risk) – examples this week include:

- YGG – 90.70% released, 326.59K tokens unlocking on a 26.56M market cap.

- BIM – 88.31% released, 74.58K tokens unlocking on a 34.18M cap.

- TRIBL – 87.99% released, 643.13 tokens unlocking on a very large 682.22M cap.

- GAU – 87.11% released, 319.8 tokens unlocking on a 103.64K cap.

- SVL – 86.34% released, 67.64K tokens unlocking on a 26.45M cap.

These profiles suggest the bulk of dilution has already occurred, so current unlocks function more as incremental emissions than cliff-style events.

Early-stage vesting (higher structural risk over time) – where less than 30% of supply is live:

- CYPR – Only 9.85% released, 16.45K tokens unlocking on a 1.05M market cap.

- ATH – 18.45% released, 10.70K tokens unlocking on a 541.41K cap.

- XPL – 22.32% released, 8.11M tokens unlocking on a 204.68M cap.

- MIRA – 22.47% released, 812.61K tokens unlocking on an 18.97M cap.

- H – 25.16% released, 9.68M tokens unlocking on a 167.93M cap.

For these tokens, vesting schedules will keep shaping performance well into 2027, and unlock weeks tend to act as significant catalysts. The histogram of released supply clearly shows a broad cluster between ~40–80% with tails into sub-25% and above 85%, reinforcing this split.

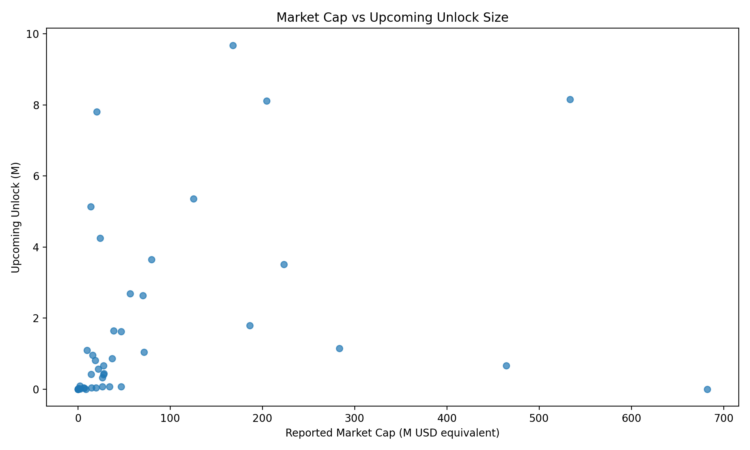

Market-cap vs unlock size

A scatter plot of reported market cap against upcoming unlock value helps categorize tokens into rough impact buckets for this week’s calendar.

Market Cap vs Unlock Value (Mar 23–29, 2026):

- Large-cap, large unlock: H, JUP, XPL, MON, FET, and SAHARA anchor the upper-right portion, combining meaningful unlocks with sizeable market caps that typically have deeper liquidity.

- Mid-cap, chunky unlock: PARTI, SOSO, UDS, VENOM, ALT, AERO, BIGTIME, and ZORA form a cluster where unlocks are material versus project size, creating fertile ground for short-term volatility when order books are not thick.

- Micro-cap, small unlock: Names like GAU, WIFI, GGP, FT, SLF, DICE, NYAN, and CYPR sit low on both axes; while absolute dollars are small, these events can still overwhelm thin markets and appeal to high-beta event traders.

This visualization makes it easier to see where unlocks are likely to be absorbed versus where they may disproportionately impact local liquidity.

Detailed token highlights

DeFi, liquidity, and infra-adjacent names

Several projects in this batch relate to DeFi, liquidity management, or infrastructure-style narratives:

- VENOM – 1.62M unlocking at 0.022 USD, on a 46.91M USD cap with 36.89% released, implying continued float expansion in an early-to-mid stage profile.

- ALT – 1.64M unlock at 0.006817 USD on a 38.80M USD cap, with 56.72% already released, reflecting a mid-curve emission.

- AERO – 1.15M unlocking at 0.306 USD on a 283.56M USD cap, 61.54% released, suggesting that tokenomics are gradually transitioning from structural risk to incremental emissions.

- CELO – 0.06661M unlocking on a 46.74M USD cap with 59.50% released, another case where remaining vesting is meaningful but no longer dominant.

AI and data-centric plays

AI-linked names remain present in this week’s unlock slate:

- FET – 657.31K tokens unlocking at 0.206 on a 464.54M cap with 80.29% released, a late-stage profile where emissions are still noticeable but float is mostly live.

- AGIX – 565.98K tokens unlocking at 0.091 on a 22.34M cap with 79.19% released, similarly advanced in its vesting path.

- GTAI – 16.33K tokens unlocking at 0.025 on a 1.02M cap with 89.68% released, firmly in “residual emission” territory.

- SOPH – 411.90K tokens unlocking at 0.009068 on a 27.83M cap with 29.82% released, still early enough that tokenomics play a significant role in near-term price.

Gaming, NFTs, and metaverse

Gaming-adjacent names appear again in this week’s calendar, though with smaller dollar sizes than the prior example article:

- BIGTIME – 4.25M unlocking at 0.013 USD on a 24.11M USD cap with 41.61% released, making it one of the higher-beta gaming events in the cohort.

- YGG – 326.59K at 0.037 USD on a 26.56M USD cap, 90.70% released, showing a largely mature float where unlocks are incremental.

- TREE – 1.09M at 0.063 USD on a 9.85M USD cap with 32.05% released, aligning with a relatively early vesting phase.

- GFAL – 41.40K at 0.001171 USD on a 6.15M USD cap, 65.90% released, a mid-to-late gaming tokenomics profile.

These tokens typically see speculative flow around unlocks, especially when paired with content updates, seasons, or NFT mints that can counterbalance supply with fresh demand.

Micro-caps and tail-risk names

At the bottom of the market-cap spectrum, several tokens combine small absolute unlock values with the potential for outsized percentage moves:

- NYAN – 1.06K tokens unlocking at 0.000538 on a 78.89K cap with 25.41% released.

- GAU – 319.8 tokens unlocking at 0.000273 on a 103.64K cap with 87.11% released.

- WIFI – 1.59K tokens unlocking at 0.000382 on a 225.25K cap with 83.19% released.

- FT – 638.97 tokens unlocking at 0.0023 on a 201.21K cap with 98.89% released.

- SLF – 987.56 tokens unlocking at 0.000499 on an 83.15K cap with 68.67% released.

- DICE – 879.32 tokens unlocking at 0.000879 with no reported market cap, highlighting data gaps but likely thin liquidity.

Market implications and sector view

Unlocks add incremental sell-side pressure to spot markets, particularly when vested allocations belong to early investors, teams, or funds that regularly recycle into liquidity. For this week:

- H, JUP, XPL, PARTI, and SOSO form the core watchlist, given their unlock size and narrative relevance across infra and DeFi-like exposure.

- Mid-caps such as UDS, SAHARA, VENOM, ALT, AERO, BIGTIME, and ZORA may see amplified volatility relative to their size when unlocks materially exceed typical daily volumes.

- Late-stage names like FET, AGIX, YGG, BIM, TRIBL, GAU, NAVX, and SVL are less about overhang and more about whether fundamentals justify valuations now that most of the float is live.

Sector-wise, the XLSX naturally clusters into:

- DeFi / liquidity / collateral: VENOM, ALT, AERO, CELO, UDS, TREE, parts of PARTI and SOSO’s usage.

- L1 / L2 / infra: H (infra-style), MON, FET, CELO, AURORA, AVAIL, NAVX, ZORA.

- AI / data: FET, AGIX, GTAI, SOPH.

- Gaming / metaverse / NFTs: BIGTIME, YGG, TREE, GFAL, ANIME, SVL.

- Micro-cap experiments: GAU, WIFI, FT, SLF, NYAN, CYPR, DICE, STIK (cap missing but likely small).

For sector-level investors, this week’s unlocks offer a chance to fine-tune exposure trimming into heavy upcoming emissions, or planning to accumulate post-event in projects with solid fundamentals but temporary tokenomics noise, making the Upcoming Token Unlocks in March 2026 an important period to monitor closely.

AI Disclosure: Cryip uses AI-assisted tools to help refine language — correcting spelling and grammar and simplifying complex terms for readability.

We do this to make crypto topics easier to understand for readers at all experience levels. AI does not draft facts, sources, or conclusions. Every article is reviewed and approved by a human editor before publication. Read our full AI Use & Content Policy.

{kind=link}