Between April 13 – 19, 2026, 35 tokens are scheduled to unlock fresh vested supply, spanning infrastructure, DeFi, gaming, and micro‑cap experiments. For each token, the price as of April 13, 06:10 AM UTC, reported market cap, the percentage of maximum supply already released, and the upcoming unlock value for this week are included. The projects are set to release $61.66M worth of tokens (USD‑equivalent), with an average float maturity of about 57.00% and a median of 56.71% of max supply already circulating. Large‑cap and high‑attention names CONX, ARB, STRK, DBR, SEI, and ZK anchor the headline unlocks, while a long tail of DeFi, gaming, and infra‑adjacent tokens contributes localized volatility and niche event‑driven opportunities.

Top unlocks by value

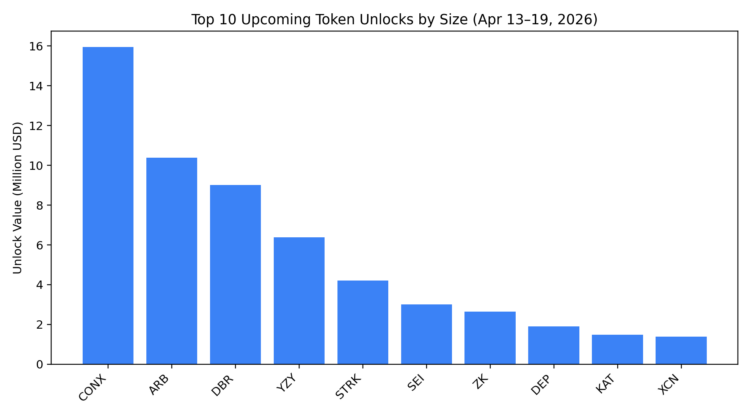

The top 5 tokens by upcoming unlock size for April 13–19, 2026 are:

- CONX carries the week’s largest unlock at approximately $15.95M against a reported market cap of $30.61M, with 87.28% of max supply already circulating. This late‑curve profile means most structural dilution is behind the market, but the absolute size of this event remains large relative to project value and can drive significant order‑book pressure if recipients monetize allocations.

- ARB unlocks around $10.38M on a $675.33M market cap with 53.07% released, placing it in a mid‑curve zone where emissions still shape ownership dispersion and float. As a large‑cap with deeper liquidity, markets may absorb supply more efficiently, yet unlock‑day flows can still widen spreads and elevate intraday volatility.

- DBR features a $9.01M unlock at a market cap near $68.73M and 47.93% released, implying a chunky event relative to project size with roughly half the total supply still to come over time. This configuration often amplifies price sensitivity, particularly if typical daily trading volumes are modest.

- STRK adds a $4.20M unlock to a $188.09M capitalization with just 30.12% of supply live, highlighting an early‑to‑mid vesting curve where tokenomics remain a primary driver of performance. Each unlock meaningfully increases the circulating float, and investor focus typically centers on whether new supply is locked, staked, or sold into spot markets.

- SEI rounds out the top group with $3.01M unlocking on a $364.17M cap and 56.93% released, a mid‑curve profile where emissions remain material but a majority of float is already circulating. As with other infra‑adjacent names, depth of derivatives and spot liquidity can help digest flows, but order‑book imbalances around the event are still likely.

Just below this top tier sit ZK (~$2.64M), SOLV (~$0.82M), IOTA (~$0.68M), PIXEL (~$0.65M), WCT (~$0.66M), and CYBER (~$0.74M), which collectively thicken the mid‑range of the week’s unlock distribution.

CONX dominates in absolute terms, followed by ARB and DBR, while STRK, SEI, ZK, SOLV, IOTA, PIXEL, and WCT form a strong second tier of events that can still drive meaningful trading activity around their respective unlock windows.

High and low supply impact

The Released Percentage shows how far each token is through its vesting lifecycle, offering crucial insights for a tokenomist assessing long-term emission schedules and structural dilution.

Late‑stage vesting (lower structural risk) – examples this week include:

- GAL – 88.83% released, $186.18K unlocking on a $40.89M market cap.

- TRIBL – 89.43% released, $428.44 unlocking on a $682.22M cap, effectively a residual emission despite the large fully‑diluted footprint.

- SVL – 86.71% released, $65.01K unlocking on a $24.92M cap.

- DEP – 82.32% released, $1.91M unlocking on a $30.90M cap, a sizeable event but with most long‑term dilution already realized.

- HTM – 80.99% released, $25.86K unlocking on a $0.98M cap.

These profiles suggest the bulk of structural dilution has already played out; current unlocks behave more like incremental emissions than cliff‑style events that shock the float.

Early‑stage vesting (higher structural risk over time) – where less than ~30% of supply is live:

- CYPR – only 10.12% released, $20.54K unlocking on a $0.88M market cap, a classic early‑curve micro‑cap.

- KAT – 23.42% released, $1.49M unlocking on an $18.43M cap, making each event meaningful relative to circulating float.

- YALA – 24.66% released, $5.71K unlocking on a $0.16M cap, where even small unlocks can move price in thin markets.

- NYAN – 26.00% released, $2.88K unlocking on an $84.11K cap.

- ZK – 28.58% released, $2.64M unlocking on a $146.70M cap, indicating a long runway of emissions ahead.

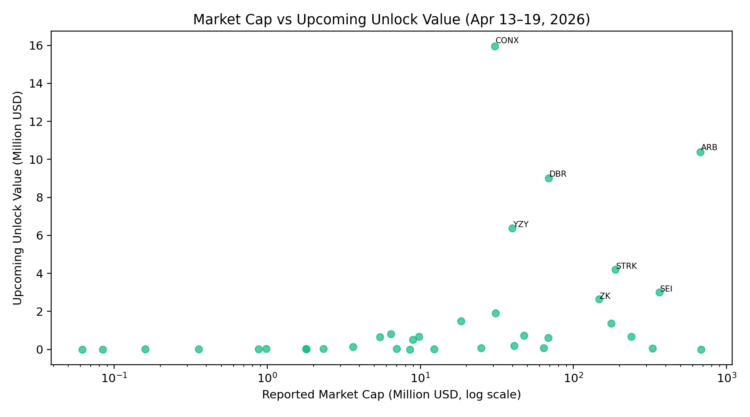

Market‑cap vs unlock size

A cross‑section of reported market cap versus upcoming unlock value helps categorize tokens into rough impact buckets for this week’s calendar.

In this log‑scale scatter:

- Large‑cap, large unlock – ARB, SEI, STRK anchor the upper band, combining meaningful unlocks with sizeable market caps and typically deeper liquidity pools.

- Mid‑cap, chunky unlock – DBR, ZK, IOTA, SOLV, PIXEL sit in a zone where events are material versus project size, creating fertile ground for short‑term volatility.

- Micro‑cap, small unlock – names like NYAN, YALA, VRTX, GSWIFT, and CYPR sit low on both axes; while absolute dollars are small, even modest sell programs can overwhelm thin order books.

This visualization makes it easier to see where unlocks are likely to be digested by robust secondary markets versus where they may disproportionately impact local liquidity and slippage.

Detailed token highlights

DeFi, liquidity, and infra‑adjacent names

Several projects in this batch relate to DeFi, liquidity, or infrastructure‑style narratives, where unlocks can influence governance participation, incentives, or restaking economics:

- AERO – $51.87 unlocking at $0.355 on a $328.38M cap with 61.67% released, suggesting emissions remain meaningful but the float is majority live.

- SEI – $3.01M unlocking at $0.054 on a $364.17M cap with 56.93% released, a core infra‑adjacent asset with continued schedule‑driven supply.

- ARB – $10.38M unlocking at $0.112 on a $675.33M cap with 53.07% released, central to L2 and DeFi stack positioning.

- SOLV – $817.66K unlocking at $0.004311 on a $6.40M cap with 34.54% released, implying ongoing float build‑out.

- W – $607.06K unlocking at $0.012 on a $68.38M cap with 56.71% released.

These tokens are often deployed for ecosystem incentives, liquidity mining, or staking, so unlocks can both pressure price and re‑fuel protocol growth initiatives depending on how allocations are used.

Scaling, data, and ZK‑linked plays

This week includes several names adjacent to scaling, infra, and zero‑knowledge narratives:

- CYBER – $737.66K unlocking at $0.832 on a $47.41M cap with 65.07% released, a mid‑to‑late curve profile where emissions remain notable.

- XCN – $1.38M unlocking at $0.004661 on a $176.03M cap with 78.49% released, reflecting an advanced vesting stage with residual but still visible dilution.

- ZK – $2.64M unlocking at $0.015 on a $146.70M cap with 28.58% released, indicating a long vesting runway intersecting with ZK‑scaling narratives.

- ZKJ – $520.93K unlocking at $0.019 on an $8.94M cap with 47.66% released, sitting mid‑curve with material emissions relative to size.

Gaming, NFTs, and metaverse

Gaming‑adjacent names appear again this week, mixing mid‑curve and late‑curve tokenomics:

- SVL – $65.01K unlocking at $0.014 on a $24.92M cap with 86.71% released, a late‑stage gaming‑style profile with incremental emissions.

- PYR – $10.30K unlocking at $0.262 on a $12.30M cap with 64.84% released, mid‑to‑late curve with continued incentive capacity.

- PIXEL – $645.48K unlocking at $0.007079 on a $5.45M cap with 52.91% released, where unlocks can meaningfully intersect with NFT or in‑game activity.

These tokens often see speculative flows around unlocks, especially when coupled with in‑game updates, seasons, or NFT drops that can offset supply with fresh demand.

Micro‑caps and tail‑risk names

At the bottom of the market‑cap spectrum, several tokens combine small absolute unlock values with the potential for outsized percentage moves:

- NYAN – $2.88K unlocking at $0.000575 on an $84.11K cap with 26.00% released.

- YALA – $5.71K unlocking at $0.000558 on a $159.02K cap with 24.66% released.

- VRTX – $121.90 unlocking at $0.000117 on a $61.83K cap with 69.09% released.

- GSWIFT – $4.16K unlocking at $0.00077 on a $356.12K cap with 42.96% released.

- CYPR – $20.54K unlocking at $0.0089 on an $877.86K cap with just 10.12% released.

Market implications and sector view

Unlocks add incremental sell-side pressure to spot markets, particularly when vested allocations belong to early investors, teams, or funds rotating capital into liquidity. In this context, this week’s tokenomics vesting updates provide critical insights into emission schedules, supply overhang, and potential price volatility. In this week’s calendar, CONX, ARB, STRK, DBR, SEI, and ZK form the core watchlist given their unlock size, vesting stage, and relevance across infrastructure and DeFi exposure. Mid‑caps such as IOTA, SOLV, PIXEL, KAT, and XCN may see amplified volatility relative to their size when unlocks materially exceed typical daily volumes. Late‑stage names like GAL, TRIBL, SVL, DEP, and HTM are less about long‑term overhang and more about whether fundamentals justify valuations now that most of the float is already live.

Sector‑wise, the week naturally clusters into:

- DeFi / liquidity / collateral: AERO, ARB, SEI, SOLV, W, CYBER.

- Infra / L1–L2–scaling‑adjacent: STRK, ARB, SEI, ZK, ZKJ, XCN, IOTA.

- Gaming / NFTs / metaverse: SVL, PYR, PIXEL and related ecosystem plays.

- Micro‑cap experiments: NYAN, YALA, VRTX, CYPR, GSWIFT and similar small‑cap names with thin books.

For sector‑level investors, this week’s unlocks provide an opportunity to fine‑tune exposure, either trimming into heavy upcoming emissions or planning to accumulate post‑event in projects with solid fundamentals but temporary tokenomics noise. In combination with the broader April unlock calendar, the April 13–19 window is an important period to monitor closely for liquidity shifts, volatility spikes, and narrative‑driven repricing across the mid‑cap and large‑cap spectrum.

{kind=link}