Between March 16 and 22, 2026, the Web3 and broader digital-asset ecosystem saw a mix of mega-acquisitions, late-stage growth rounds, and select early-stage financings, with disclosed capital dominated by M&A and later-stage deals. Activity clustered around March 17, when several strategic and growth transactions closed on the same day.

Key weekly highlights

- Total disclosed capital reached approximately 3.28 billion USD across the week.

- M&A and late-stage financings (BVNK, Kalshi, Metaplanet) accounted for the bulk of disclosed volume, highlighting continued consolidation and institutional interest.

- The single largest transaction was the acquisition of BVNK by Mastercard, valued at around 1.8 billion USD.

- Other large tickets included Kalshi’s 1.0 billion USD Series E, Metaplanet’s 255 million USD Post-IPO capital, and Bluesky’s 100 million USD Series B.

- Early-stage activity was visible but comparatively modest in dollar terms, led by Keyban’s pre-seed and multiple seed/early deals with undisclosed amounts.

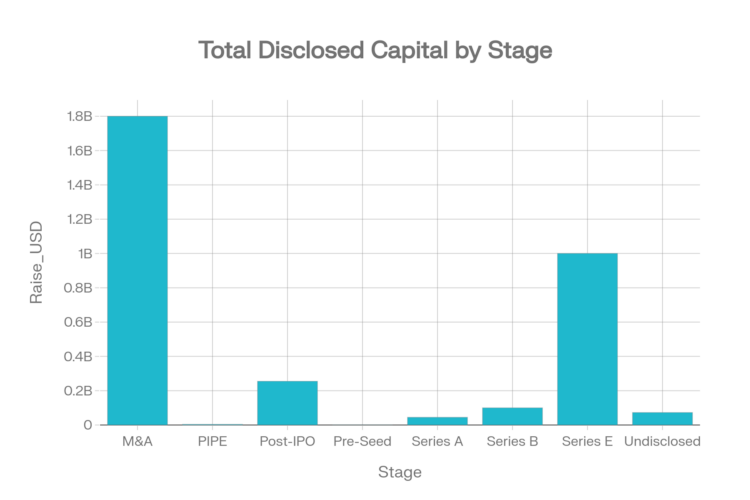

Capital distribution by stage

Disclosed capital was heavily skewed toward M&A and late-stage rounds, with early-stage pre-seed and Series A rounds contributing a much smaller share in absolute terms.

| Stage | Disclosed amount (USD) |

|---|---|

| M&A | 1,800,000,000 |

| Series E | 1,000,000,000 |

| Post-IPO | 255,000,000 |

| Series B | 100,000,000 |

| Undisclosed | 72,600,000 |

| Series A | 45,200,000 |

| PIPE | 3,450,000 |

| Pre-Seed | 572,330 |

The dominance of M&A and Series E capital reflects a maturing market where strategic consolidation and later-stage scale-ups continue to attract the largest tickets. Meanwhile, Series A and pre-seed funding numbers suggest ongoing pipeline development, but with far smaller absolute amounts relative to headline late-stage deals.

1. Strategic M&A and consolidation

- BVNK (acquired by Mastercard) – M&A, 1.80 billion USD, March 17

BVNK’s acquisition by Mastercard was the largest transaction of the week, underscoring traditional finance’s push deeper into digital asset infrastructure and embedded crypto banking. The deal likely strengthens Mastercard’s positioning in crypto-friendly payments, settlement, and treasury solutions targeting both enterprises and fintechs. - Rarible (acquired by Impossible) – M&A, amount undisclosed, March 20

Rarible, a well-known NFT marketplace, entered an M&A transaction with Impossible, signaling continued strategic repositioning in the NFT and creator-economy vertical. Undisclosed terms suggest a focus on product and ecosystem synergies rather than headline valuation. - Brahma (acquired by Polymarket) – M&A, amount undisclosed, March 18

Brahma’s acquisition by Polymarket points toward a deeper integration of DeFi strategies and on-chain prediction markets, potentially improving liquidity, risk management, and structured products around event markets. - Genpaid (acquired by Sokin) – M&A, amount undisclosed, March 17

Genpaid’s deal with Sokin highlights ongoing consolidation in cross-border payments and remittance solutions built on or adjacent to Web3 rails. - Architech & Autonomous (acquired by GSR) – M&A, amounts undisclosed, March 17

GSR’s dual acquisitions emphasize the importance of trading, market-making, and infrastructure capabilities to institutional crypto liquidity providers. These moves likely expand GSR’s technology stack and product breadth.

Overall, the week’s M&A slate indicates aggressive positioning by both Web2 financial incumbents and crypto-native liquidity providers to control critical infrastructure layers in payments, trading, and NFT markets.

2. Late-stage growth and public-market capital

- Kalshi – Series E, 1.00 billion USD, led by Coatue Management (March 19)

Kalshi’s 1.0 billion USD Series E represents a major late-stage bet on event-based trading platforms and prediction markets. Backing from Coatue Management reflects growing institutional comfort with regulated venues bridging traditional derivatives and on-chain market structures. - Metaplanet – Post-IPO, 255 million USD (March 16)

Metaplanet’s post-IPO capital raise has secured $255 million, strengthening its financial position to support further expansion and potential Web3-native strategic investments. The transaction highlights how publicly listed entities continue to serve as active channels for capital formation within the broader digital assets ecosystem. - Bluesky – Series B, 100 million USD, with Bain Capital Crypto, Alumni Ventures and 4 others (March 19)

Bluesky’s 100 million USD Series B underscores continued investor conviction in decentralized social and identity layers. Backing from Bain Capital Crypto and others shows that social protocols and infrastructure remain key themes despite broader market cycles. - Ironlight – Series A, 21 million USD, backed by Gregory Braca and 2 others (March 16)

Ironlight’s Series A round, raising 21 million USD, indicates investor appetite for infrastructure or application-layer plays that are early but already demonstrating product–market fit.

3. Mid-stage and growth rounds

- TransFi – Series A, 14.2 million USD, led by Turing Financial Group (March 17): TransFi’s 14.2 million USD raise reflects sustained momentum in cross-border on/off-ramp and payment-rail solutions that connect fiat and crypto liquidity.

- dtcpay – Series A, 10 million USD, backed by Vertex Ventures (March 17): dtcpay’s 10 million USD Series A strengthens its capacity to scale crypto-payment acceptance and settlement infrastructure, particularly for merchants and platforms needing multi-currency support.

These rounds highlight strong investor focus on real-world payments and financial connectivity, areas where Web3 rails can deliver clear efficiency gains.

4. Undisclosed-amount strategic deals

- Avalanche – undisclosed, Animoca Brands (March 19): An undisclosed strategic transaction involving Avalanche and Animoca Brands reinforces Avalanche’s role as a high-performance chain for gaming, NFTs, and consumer apps, backed by a leading Web3 gaming investor.

- Current – undisclosed, OKX Ventures and 4 others (March 17): Current’s undisclosed deal with OKX Ventures and others suggests deeper integration between consumer-facing products and exchange/infrastructure providers.

- Derivio – undisclosed, YZi Labs (prev. Binance Labs) and 6 others (March 17): Derivio’s raise from YZi Labs and others points to continued innovation in derivative and structured products built around on-chain assets.

- Stripe – 14.6 million USD labelled as Undisclosed stage, from Robinhood (March 17): Although categorized under “Undisclosed” as a stage, this 14.6 million USD strategic capital event between Stripe and Robinhood highlights deepening ties between fintech platforms and digital-asset rails.

- Republic – undisclosed, backed by Hamilton Lane (March 17): Republic’s deal with Hamilton Lane signals ongoing institutionalization of private-market and crowdfunding platforms with blockchain-enabled infrastructure.

Collectively, these transactions, even without full financial transparency, show high strategic intensity around gaming, payments, derivatives, and capital formation platforms.

5. Early-stage and emerging players

- Keyban – Pre-Seed, 572,330 USD, Not Set investors (March 17): Keyban’s pre-seed round of approximately 572,330 USD illustrates steady early-stage activity, likely in infrastructure or vertical applications that are just beginning their growth journey.

- Lendasat – Pre-Seed, amount undisclosed, backed by Fulgur Ventures and 2 others (March 17): Lendasat, supported by Fulgur Ventures and others, suggests investor interest in credit, lending, or financial data solutions with a Web3 angle.

- MYRIAD – Seed, amount undisclosed, backed by Everest Ventures Group (EVG) and others (March 19): MYRIAD’s seed round from EVG and over two dozen other backers signals strong syndicate interest and potential for rapid ecosystem integration.

AI Disclosure: Cryip uses AI-assisted tools to help refine language — correcting spelling and grammar and simplifying complex terms for readability.

We do this to make crypto topics easier to understand for readers at all experience levels. AI does not draft facts, sources, or conclusions. Every article is reviewed and approved by a human editor before publication. Read our full AI Use & Content Policy.

{kind=link}