- $1 billion convertible notes repurchased at ~9% discount

- $88.1 million value captured from discounted buyback

- Convertible debt reduced by approximately 30%

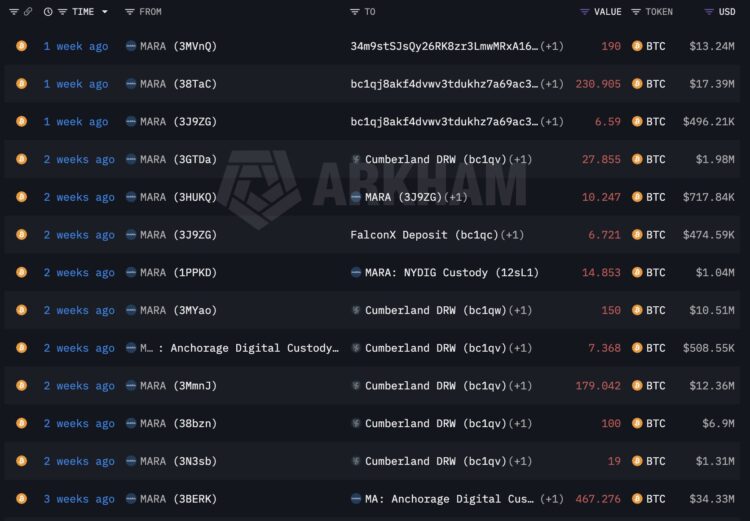

- Bitcoin sales of 15,133 BTC generated $1.1 billion

- Total convertible debt drops from $3.3B to $2.3B

- Company faces $3.65B total debt vs $3.15B market cap

MARA Holdings, Inc. (NASDAQ: MARA) announced agreements to repurchase approximately $1 billion in aggregate principal amount of its 0.00% convertible senior notes due in 2030 and 2031 at a discount to par value.

The company will repurchase:

- $367.5 million of 2030 notes for approximately $322.9 million

- $633.4 million of 2031 notes for approximately $589.9 million

The transactions reflect an approximate 9% discount and are expected to close on March 30 and March 31, 2026, subject to customary conditions.

Following completion, MARA’s outstanding convertible notes will decrease significantly, leaving:

- $632.5 million of 2030 notes

- $291.6 million of 2031 notes

Total convertible note debt will decline from $3.3 billion as of December 31, 2025, to approximately $2.3 billion.

Bitcoin Sales Fund Strategy

To finance the repurchase, MARA disclosed that it sold 15,133 bitcoin between March 4 and March 25, 2026, generating approximately $1.1 billion. The proceeds are being used primarily to fund the debt buyback, with any remaining funds allocated for general corporate purposes.

According to CEO Fred Thiel, the strategy enabled the company to capture approximately $88 million in value, reduce potential shareholder dilution, and use its bitcoin holdings to deleverage the balance sheet.

Financial Position and Market Context

The company’s financial position reflects ongoing pressure, with total debt standing at $3.65 billion compared to a market capitalization of $3.15 billion as of Q4 2025.

Key financial indicators include:

- Debt-to-equity ratio of 1.05

- Negative levered free cash flow of $1.36 billion over the past twelve months

MARA’s stock has declined 49% over the past six months and was recently trading at $8.28, with high volatility indicated by a beta of 5.42. Analyst updates reflect a more cautious outlook. Clear Street reduced its price target from $16 to $9, citing a lower EBITDA estimate of $99 million for 2027. Cantor Fitzgerald also lowered its target from $21 to $11 while maintaining an Overweight rating.

Recent quarterly results showed a 20% decline in mining revenue quarter-over-quarter and negative adjusted EBITDA. Despite these challenges, the stock saw a 6% increase amid a broader rebound in cryptocurrency-related equities alongside rising Bitcoin prices. J. Wood Capital Advisors LLC acted as financial advisor, while Paul, Weiss, Rifkind, Wharton & Garrison LLP served as legal advisor for the transactions.

{kind=link}