The stablecoin market has evolved far beyond a single-chain affair. With over a dozen major blockchain networks vying for stablecoin liquidity, the distribution of supply across chains tells a powerful story about where real economic activity is taking place and which networks are winning the race. This analysis examines the blockchain network distribution of 10 leading stablecoins: USDT, USDC, USDS, USDe, USD1, DAI, PYUSD, BUIDL, USDf, and USYC.

Ethereum Remains the Default But It’s Not Universal

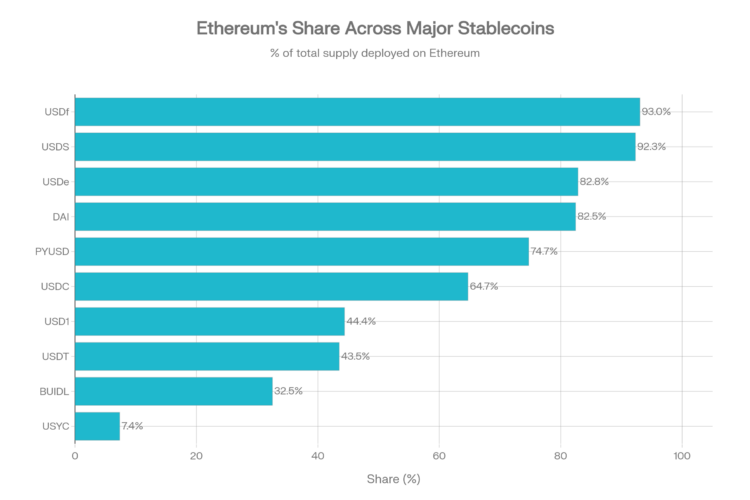

Ethereum continues to be the single most important chain for stablecoins, but its dominance varies wildly depending on the token. Falcon USD (USDf) is the most Ethereum-concentrated at 93.05%, followed closely by Sky Dollar (USDS) at 92.30%. At the other end of the spectrum, Circle’s USYC places just 7.37% on Ethereum, with the vast majority (92.63%) on BSC.

This divergence matters. Stablecoins deeply tied to DeFi governance and institutional use cases USDS, DAI (82.45%), USDe (82.84%) gravitate toward Ethereum for its mature smart contract infrastructure. Meanwhile, newer entrants like USYC and BUIDL (32.51% on Ethereum) are deliberately pursuing multi-chain or alternative-chain strategies from day one.

USDT vs USDC: A Tale of Two Distribution Strategies

The two largest stablecoins by market cap Tether (USDT) and USD Coin (USDC) reveal fundamentally different network strategies.

USDT is split almost evenly between Tron (45.86%) and Ethereum (43.52%), with BSC (4.88%) a distant third. This reflects USDT’s heavy use in peer-to-peer transfers, remittances, and exchange settlement activities where Tron’s low fees give it a significant edge.

USDC, by contrast, is Ethereum-first at 64.72%, with meaningful secondary presence on Solana (11.49%), Base (5.78%), and Hyperliquid L1 (5.59%). USDC’s distribution mirrors the DeFi and institutional on-chain trading ecosystem chains where programmable money flows through smart contracts rather than simple transfers.

The key takeaway: USDT follows the payments narrative (Tron); USDC follows the DeFi and trading narrative (Ethereum + Solana + Base).

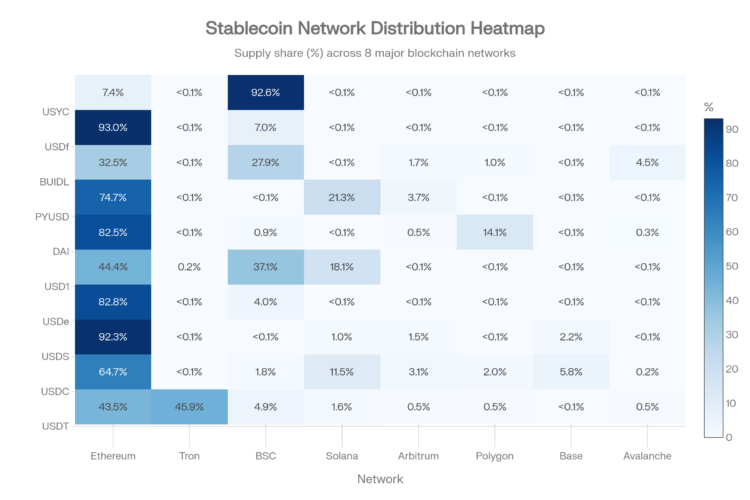

Stablecoin × Network Heatmap

The heatmap below reveals the complete distribution matrix which stablecoins are present on which chains, and at what concentration.

Several patterns emerge from this matrix:

-

Ethereum is the only chain that hosts all 10 stablecoins, ranging from 7.37% (USYC) to 93.05% (USDf).

-

BSC is the second most diversified chain, attracting meaningful supply from USDT, USDe, USD1, BUIDL, USDf, and USYC.

-

Solana has carved a niche as the preferred secondary chain for payment-oriented stablecoins (PYUSD at 21.27%, USD1 at 18.09%, USDC at 11.49%).

-

Tron is important for USDT but largely irrelevant for everything else only USDT and USD1 (0.18%) have any presence on Tron.

-

Polygon finds significant usage only through DAI (14.06%) and minor presence in USDT, USDC, and BUIDL

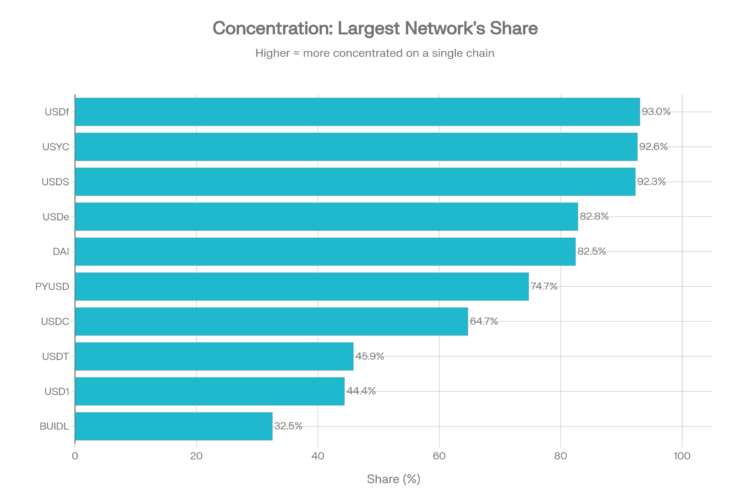

Concentration Risk: Which Stablecoins Are Single-Chain Dependent?

Not all multi-chain strategies are created equal. Some stablecoins remain overwhelmingly reliant on a single network, creating concentration risk if that chain experiences congestion, outages, or regulatory pressure.

The data reveals three tiers of concentration:

| Tier | Stablecoins | Dominant Network Share | Risk Level |

|---|---|---|---|

| Highly Concentrated | USDf (93.1%), USYC (92.6%), USDS (92.3%) | >90% on one chain | High |

| Moderately Concentrated | USDe (82.8%), DAI (82.5%), PYUSD (74.7%), USDC (64.7%) | 65-85% on one chain | Medium |

| Distributed | USDT (45.9%), USD1 (44.4%), BUIDL (32.5%) | <50% on top chain | Lower |

BlackRock’s BUIDL is the most evenly distributed stablecoin in the dataset, with Ethereum (32.51%), Aptos (30.87%), and BSC (27.90%) each holding roughly a third of supply. This three-way split likely reflects BlackRock’s institutional approach to risk diversification across chains.

World Liberty Financial USD (USD1) also shows notable distribution across three chains Ethereum (44.40%), BSC (37.06%), and Solana (18.09%) suggesting a deliberate multi-ecosystem growth strategy. This growth is increasingly driven by modern cross-chain protocols; for instance, you can explore how the LayerZero cross-chain ecosystem facilitates such seamless asset movement between these diverse networks.

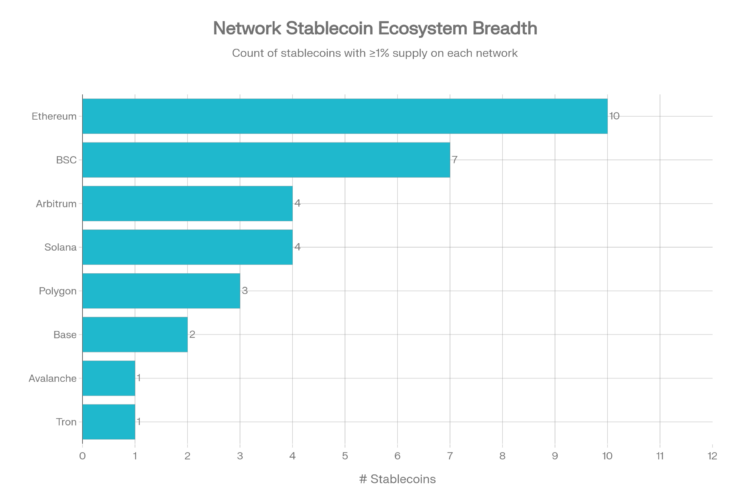

Which Blockchains Have the Broadest Stablecoin Ecosystems?

Flipping the lens, we can ask: which networks attract the most diverse set of stablecoins? The chart below counts how many of the 10 stablecoins maintain at least 1% of their supply on each chain.

Ethereum leads with 9 out of 10 stablecoins having meaningful (≥1%) supply on the network. BSC comes in second, with 5 stablecoins holding at least 1% of supply there. Solana hosts 3 stablecoins at the 1% threshold. Meanwhile, chains like Avalanche, Base, and Polygon each attract 1-2 stablecoins at meaningful levels.

This ecosystem breadth metric matters for DeFi composability. Networks with a wider range of stablecoins can offer more diverse lending, borrowing, and trading opportunities creating a virtuous cycle that attracts further liquidity.

Key Findings and Implications

1. Ethereum’s moat is deep but not impenetrable. It remains the default home for stablecoins, especially those tied to DeFi protocols and institutional use cases. But chains like BSC, Solana, and even Aptos are carving out meaningful niches.

2. The USDT-Tron alliance is unique. No other stablecoin has replicated USDT’s massive Tron presence. This reflects Tron’s specialization as a low-cost transfer rail rather than a smart contract platform.

3. Institutional stablecoins favor multi-chain from the start. BUIDL (BlackRock) and USD1 (World Liberty Financial) show deliberate three-chain diversification strategies, contrasting with the Ethereum-heavy approaches of older stablecoins.

4. Layer 2s are gaining ground but slowly. Arbitrum, Base, and OP Mainnet appear across multiple stablecoins, but typically below 5% of supply. The L2 stablecoin story is still in its early chapters.

5. Concentration risk is real. Three stablecoins USDf, USYC, and USDS have over 90% of supply on a single chain. Any disruption to that chain would disproportionately impact their usability. This data based on Defilama

{kind=link}