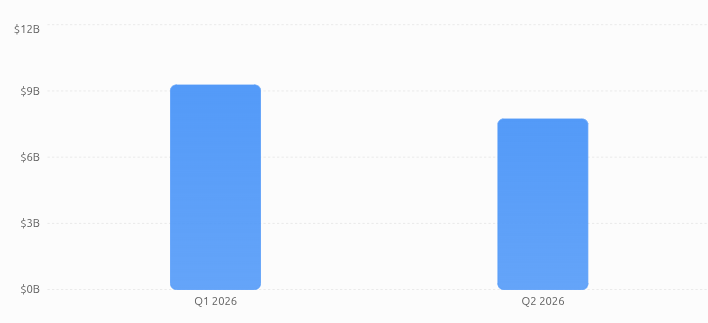

Q2 2026 recorded $7.73 billion raised across 252 web3 and crypto deals, showing only a modest pullback from Q1’s explosive $9.27B while preserving strong breadth across stages and sectors. Capital concentrated heavily in late‑stage infrastructure, exchanges, and RWA platforms, even as dozens of Seed and Pre‑Seed rounds sustained the innovation pipeline.

Across April–June, the quarter blended primary rounds (Seed to Series D and debt financings) with an intense M&A wave, confirming crypto’s transition into a strategic infrastructure layer for global finance rather than a speculative niche.

Q2 vs Q1 2026: Capital Stack Continuity

Q1 2026 delivered $9.27B across 255 deals with eight mega‑rounds (> $100M) accounting for 78% of disclosed capital and an average round size of $87.2M. Q2’s $7.73B over 252 deals keeps the ecosystem near peak velocity, but with capital distributed more evenly across large late‑stage raises and numerous mid‑range Series A/B tickets.

While Q1 was defined by a handful of billion‑dollar validations (BVNK, Kalshi, Polymarket, Core Scientific), Q2 shifts toward consolidation and scaling: fewer ultra‑mega rounds, but more frequent $20M–$350M tickets into exchanges, RWA infrastructure, and AI/data platforms. Together, Q1–Q2 confirm the new capital stack: TradFi‑anchored mega‑rounds at the top, dense seed activity at the bottom, and strategic plus M&A deals bridging the middle.

Q2 Funding Pulse: Stage and Deal Type Breakdown

Q2’s 252 deals span Pre‑Seed, Seed, Series A–D, Strategic, Private, Undisclosed, M&A, Post‑IPO, and debt‑like instruments, mirroring the sophistication seen in Q1. Seed and Pre‑Seed rounds remained abundant, with dozens of deals in the $1M–$8M range powering new exchanges, AI tools, infra protocols, and fintech rails.

On the other end of the spectrum, late‑stage Series B/C/D, Post‑IPO, and large Undisclosed tickets accounted for the majority of disclosed dollars, particularly for RWA/tokenization platforms, centralized exchanges, custody, and analytics providers. M&A deals, which were already strong in Q1 (44 transactions, $3.1B), intensified further in Q2, reinforcing the thesis of decade‑long consolidation.

Monthly Momentum: April, May, June 2026

The quarter’s web3 fundraising updates reveal a balanced ecosystem where blockbuster transactions coexist with a healthy pipeline of Seed and Pre-Seed innovation across AI, fintech, infrastructure, and regional exchanges.

April 2026: Infrastructure and Exchange Build‑Out

April’s sheet entries show a dense mix of Seed and Series A rounds alongside blockbuster Undisclosed and M&A activity. Bitnomial’s $550M M&A deal anchors the month, signaling aggressive consolidation in derivatives and institutional trading.

Additional highlights include Exponent Finance ($5M Seed), XO Market ($6M Seed), legend.trade ($3.5M Seed), Hata ($8M Series A), Liquid ($18M Series A), and Stablecoin Development Corporation ($134M Undisclosed), illustrating investors’ focus on execution venues, payment rails, and stablecoin infrastructure.

May 2026: Peak Mega‑Round Intensity

May emerges as Q2’s capital apex with multiple nine‑figure raises and heavy M&A. Dunamu logs two huge Undisclosed rounds ($204M and $667M), Kalshi returns with another $200M Undisclosed raise, SendCutSend secures $110M, Gemini raises $100M in a strategic round, Exa closes a $250M Series C, and Arc blockchain captures $222M in a Private round.

M&A continues its Q1 trajectory: DFlow ($100M M&A), Mirantis ($625M M&A), Reap ($600M M&A), Houdini Swap ($18M M&A), GAMEE ($11M M&A), TokenOps.xyz and Cometh among others, marking May as the peak month for consolidation across infra, gaming, and tooling.

June 2026: Consolidation + Early‑Stage Breadth

June balances mega‑rounds with a broad early‑stage base. Digital Asset raises $355M (Undisclosed), Morpho secures $175M (Undisclosed), Bitbank logs $289M (M&A), fomo closes a $75M Series B, Interchecks raises $50M Series C, EDGE Markets $29.2M Series A, and SignalPlus $50M Series B.

Simultaneously, June lists numerous Seed and Pre-Seed deals: Techdollar ($3M Pre-seed), Daya ($2.4M Pre-Seed), Sovra ($2M Pre-Seed), MNX ($6.4M Pre-Seed), Speed Labs ($6.5M Seed), TVL Capital ($5M Seed), plus multiple Strategic rounds for AI and infra projects (AiTraceRoot, SEALCOIN, Neura AI, Ai Pay With Crypto, Ethena, Mobius Exchange, Amiko). This mix confirms that innovation breadth didn’t slow even as large players consolidated market share.

Deal Count by Stage (Top Segments, Q2 2026)

Early‑stage breadth remained a defining feature of Q2, echoing Q1’s 57 Seed/Pre‑Seed deals. Across April–June, the spreadsheet shows dozens of Pre‑Seed and Seed deals, particularly in AI tooling, data, execution infrastructure, and region‑specific fintech.

At the same time, Strategic, Undisclosed, and M&A transactions collectively form a large share of total deal count, well over 40% of the sheet entries, underscoring that Q2’s capital wasn’t only about VC rounds but also complex balance-sheet moves and ownership transfers. Series A/B/C/D and Post-IPO deals fill out the upper mid-tier, delivering sustained growth capital into already validated businesses in custody, analytics, trading, and RWA.

The Top Deals That Defined Q2 2026

Infrastructure and institutional rails again wear the crown, with exchanges, RWA platforms, mining‑adjacent infra, and analytics dominating the largest tickets. On the basis of the XLSX:

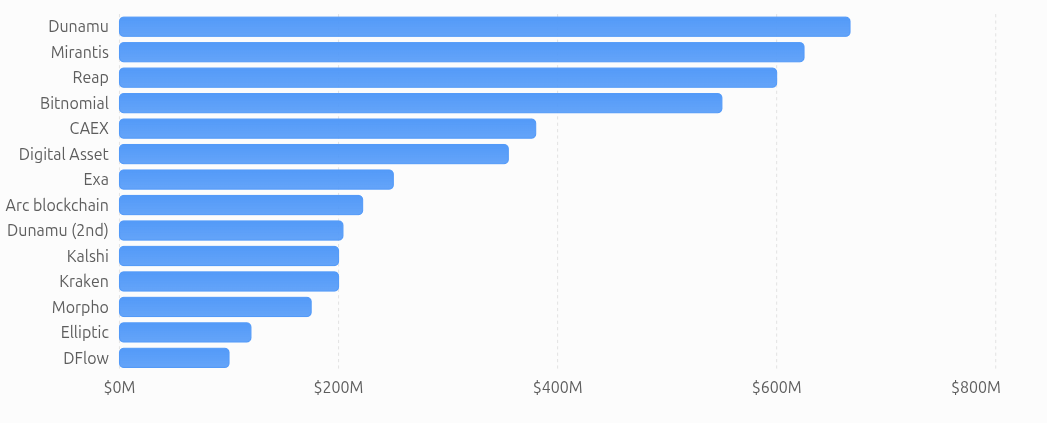

- Bitnomial – $550M (M&A): Massive derivatives venue consolidation, foreshadowing institutional futures and options depth.

- Dunamu – $667M + $204M (Undisclosed): Dual raises powering South Korea’s leading crypto infrastructure stack and regional dominance.

- Digital Asset – $355M (Undisclosed): RWA and enterprise blockchain rails scaled toward trillion‑dollar asset tokenization.

- Mirantis – $625M (M&A): Cloud‑infra and dev tooling convergence with crypto, anchoring hybrid infra for web3 workloads.

- Reap – $600M (M&A): Corporate credit and RWA integrations signal debt‑driven expansion of crypto treasury solutions.

- CAEX – $380M (Undisclosed): Centralized exchange funding reinforces post‑FTX regulatory moats and institution‑grade liquidity.

- Exa – $250M (Series C): Advanced AI and data infrastructure for crypto workflows, highlighting convergence between AI and finance.

- Kalshi – $200M (Undisclosed, follow‑on): After its Q1 $1B Series E, Q2 capital strengthens prediction markets as a long‑term asset class.

- Kraken – $200M (Undisclosed): Continued build‑out of compliant global exchange infrastructure under favorable US policy.

- Arc blockchain – $222M (Private): Large private raise for RWA/tokenization infra, extending the thesis of regulated on‑chain assets.

- Dunamu (second tranche) – $204M (Undisclosed): Reinforces the company’s role as a regional powerhouse and structural liquidity provider.

- Elliptic – $120M (Series D): Compliance and analytics cemented as system‑critical infrastructure for institutional crypto.

- DFlow – $100M (M&A): Liquidity routing and infrastructure consolidation to optimize order flow and market structure.

- Morpho – $175M (Undisclosed): Next‑generation lending protocol capitalized to compete in the post‑DeFi‑summer, RWA‑driven era.

These top deals confirm that mega‑round gravity remains firmly pointed at exchanges, RWA, mining/infra, and analytics, not speculative consumer applications.

Q2 Power Players: Investor and Acquirer Patterns

Although Q2’s file is deal‑centric rather than investor‑centric, recurring patterns mirror Q1’s capital stack. Large TradFi and institutional investors continue to anchor the biggest tickets, particularly in exchanges, mining, RWA, and prediction markets.

Strategic corporate buyers dominate M&A: Bitnomial, Mirantis, Reap, GAMEE, Houdini Swap, Amberdata, WonderFi, Helium Mobile, multiple data/analytics shops, showing that listed or near-listed companies now routinely acquire crypto plumbing instead of building it in-house. On the VC side, repeated Series A/B/C activity in AI/data (Exa, EDGE Markets, Capital B, Judgment Labs), trading infra (Onramp, OpenFX-style platforms, Spektr), and payments (WasabiCard, BetHog, Catena) indicates methodical bets on scalable revenue engines.

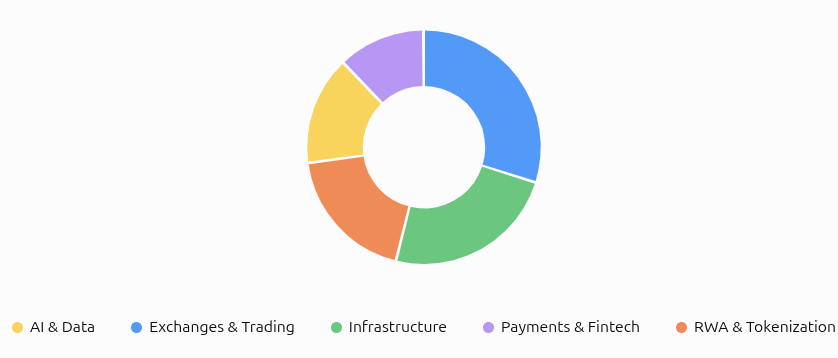

Five Strategic Themes Reshaping Crypto in Q2 2026

Q2 2026 saw capital concentrate around exchange infrastructure, real-world asset (RWA) tokenization, AI-powered blockchain services, industry consolidation through M&A, and payment infrastructure, reflecting crypto’s continued shift toward institutional-scale financial infrastructure.

1. Exchange and Trading Moats Deepen

Across April–June, capital flowed heavily into exchanges, trading venues, and execution platforms, from Bitnomial’s $550M M&A to CAEX’s $380M Undisclosed, Coinone’s $106M, Payward’s $200M, Liquid’s $18M Series A, Hata’s $8M Series A, and multiple regional venues. Post-FTX, these raises extend Q1’s narrative: centralized venues rebuild trillion-dollar liquidity moats under stricter regulation and institutional scrutiny.

Smaller Seed and Series rounds for trading tools (XO Market, legend.trade, Ouinex, OnRe Finance, IO Trader’s multiple rounds, ArcNova) show that execution innovation persists at the edge even as big exchanges entrench the core.

2. RWA and Tokenization Goes Mainstream

Stablecoin Development Corporation ($134M Undisclosed), Digital Asset ($355M Undisclosed), Arc blockchain ($222M Private), Centrifuge (Undisclosed), Reap ($600M M&A), Saturn Credit ($2M Seed), OpenTrade ($17M Strategic), Stockcoin (Seed), and multiple credit/payment platforms depict a quarter where RWA is no longer an experiment but a core funding theme. This extends Q1’s trend where debt instruments (e.g., Core Scientific’s $1B refinancing) began to dominate mining and infrastructure economics.

The implication: tokenized treasuries, on‑chain credit, and structured RWA products are becoming foundational, with Q2 capital building rails for institutions to access crypto yields through regulated wrappers.

3. AI, Data, and Analytics Arms Race

The XLSX lists a cluster of AI‑ and data‑driven projects, AEON, AnotherBall, AiTraceRoot, AIW3.ai, 2U2ai, K25.ai, K25 AI, ChimpX AI, Origin Lab, Eleutheria, AlloX, OpenRouter, SuiXi, Exa, Elliptic, EDGE Markets, Amberdata, Messari, Blockworks, Judgment Labs. Many of these deals sit between Seed and Series B/C, with tickets up to $250M (Exa) and $120M (Elliptic) reinforcing the thesis that AI‑powered analytics, risk systems, and routing will define institutional crypto workflows.

This arms race complements Q1’s data and infra bets (Talos, Upvest, prediction markets) and positions AI tooling as a horizontal layer across trading, compliance, research, and execution.

4. M&A Consolidation Accelerates Further

Q1 saw 44 M&A deals worth $3.1B, led by Mastercard–BVNK, BitGo, and others. Q2’s shows at least comparable scale, with M&A touching exchanges (Bitnomial, Bitbank, WonderFi), gaming (GAMEE), infra (Mirantis, Reap, DFlow, TokenOps.xyz, Cometh), analytics (Amberdata), DeFi tooling, and mobile (Helium Mobile).

This confirms that crypto is in a consolidation era: small to mid‑sized platforms are being absorbed into institution‑grade stacks, and acquirers view vertical integration as essential to controlling liquidity, data, and compliance pipelines.

5. Payments and Fintech Become Mission‑Critical

Payments and B2B/B2C fintech rails appear repeatedly, GoSats ($5M Series A), Saturn Credit ($2M Seed), Nuva Digital ($5.2M Seed), Transak (Undisclosed), Tazapay‑style bridges, WasabiCard ($10M Series A), Ai Pay With Crypto ($10M Undisclosed), Nomisma ($1.6M Strategic), multiple remittance and card plays.

Combined with Q1’s BVNK acquisition and Tether‑anchored payments bets, Q2 confirms that fiat‑crypto bridges are now treated as mission‑critical infrastructure: they define how consumers and institutions actually touch the asset class.

Q2 2026 vs Market History: Capital Stack Confirmed

2025 closed with 1,813 deals and $34.94B total, averaging $19.3M per round with only 12% of capital in mega‑rounds. Q1 2026 re‑architected that stack: 255 deals, $9.27B, $87.2M average round, and 78% of disclosed dollars in eight mega‑rounds.

Q2’s $7.73B across 252 deals shows that this new regime is not a one‑off; mega‑round concentration persists, but with more diversity in large tickets and heavier reliance on M&A and strategic/undisclosed structures. Under President Trump’s pro‑crypto administration and continued regulatory clarity, TradFi capital clearly treats crypto infra, RWA, and exchanges as core components of the global financial stack.

Forward Signals: Eight Predictions for Q3 2026

Based on Q2 flows and Q1–Q2 continuity:

- TradFi deepens its role as primary capital stack: Expect more CAEX/Kraken‑style raises and complex debt/private structures around mining, RWA, and exchanges.

- Prediction markets and event‑based instruments expand beyond Q1’s spike: Kalshi and Polymarket’s capital momentum will inspire copycats and structured products blending prediction markets with RWA and FX.

- Debt and credit infrastructure extend beyond mining into broader RWA: Following Core Scientific and Reap‑style moves, expect more debt financings for exchange infra, RWA, and tokenized credit platforms.

- M&A wave accelerates toward 200+ annual deals: Q1’s 44 M&A deals and Q2’s broad consolidation suggest triple‑digit annual transaction counts as TradFi buys analytics, custody, and consumer apps.

- Seed breadth remains decade‑proof: With dozens of Q2 Seed/Pre‑Seed deals across AI, infra, and local fintech, venture pipelines look resilient even if mega‑round pace oscillates.

- RWA and corporate Bitcoin treasuries proliferate: Arc blockchain, Digital Asset, Metaplanet‑style Q1 signals, and Q2 RWA focus point to more corporates allocating via tokenized structures.

- Payments and fiat‑crypto bridges remain killer apps: BVNK in Q1 plus Q2’s multiple card, remittance, and payment rounds confirm rails, not pure DeFi yield, as the dominant adoption vector.

- CEX and infra moats scale toward multi‑trillion volumes: CAEX, Coinone, Kraken, Bitnomial, Liquid, Dunamu, and others are building execution, custody, and settlement networks that look increasingly like core global financial infrastructure.

Conclusion

Q2 2026’s $7.73B across 252 deals confirms that crypto and web3 have firmly entered their strategic infrastructure era, rather than a speculative phase. Capital continues to follow a barbell pattern: mega‑rounds and large M&A into exchanges, RWA platforms, and AI/data infrastructure at the top, with dense Seed and Pre‑Seed activity sustaining long‑term innovation at the bottom.

Taken together with Q1’s $9.27B, Q2 shows that TradFi institutions now consistently anchor the largest tickets while venture capital methodically seeds the next generation of rails, execution venues, and analytics. Under supportive regulatory conditions and accelerating institutional onboarding, the winners of the coming decade will be the projects that position themselves as essential plumbing: liquidity providers, regulated payment bridges, tokenization platforms, and data/AI engines, rather than short-cycle speculative bets.

References: A full dataset for the Q2 2026 Crypto Fundraising Report is available on GitHub with detailed deal-level breakdowns and investor activity.

{kind=link}