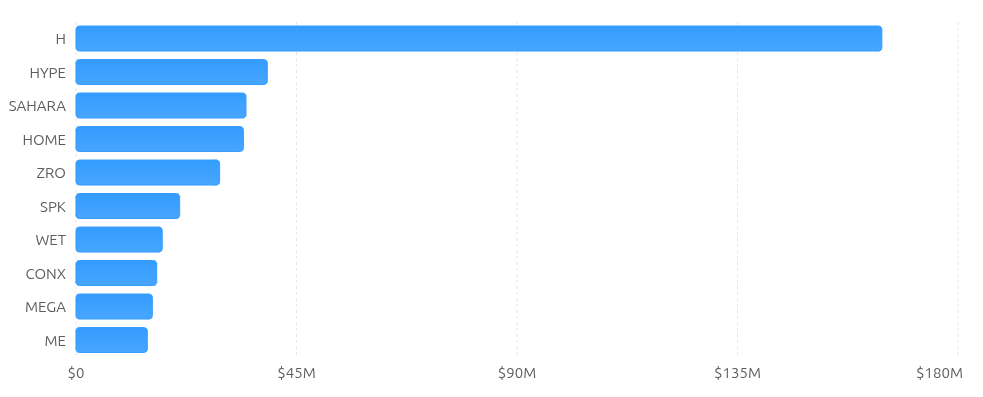

June 2026 features scheduled token unlocks for 144 tracked crypto assets, with a combined upcoming unlock value of approximately $580.33M based on prices as of June 1, 7:15 AM UTC. Unlock pressure is highly concentrated among top-tier infrastructure projects, with H Network leading at $164.46M, followed by HYPE ($39.04M), SAHARA ($34.69M), HOME ($34.16M), ZRO ($29.31M), and SPK ($21.15M) driving the majority of the month’s dollar-value supply expansion.

While this monthly total represents a moderate unlock cycle compared to multi-billion dollar waves seen in Q1 2026, the relative size of unlocks versus market cap for several mid-cap and small-cap tokens introduces material short-term dilution risk at the individual asset level. At the same time, large-cap infrastructure tokens such as HYPE, ENA, APT, ARB, and SEI face unlocks that are significant in absolute terms but modest relative to their valuations, suggesting more manageable market impact under normal liquidity conditions.

HYPE Note: The crossed-out value reflects the original whitepaper unlock estimate. The highlighted value represents the amount currently committed by the team for unlocking. These figures may differ, as projects frequently adjust token allocations, vesting schedules, or claim amounts prior to the unlock event.

Major Token Unlock Events

Top-Tier Unlocks ($10M+ Range)

The top-tier category this month is dominated by a select group of tokens whose individual unlocks fall in the high-double-digit millions of dollars, collectively accounting for approximately 65% of the $580.33M monthly total.

H Network – $164.46M unlock: H has the single largest unlock of the month at approximately $164.46M, against a reported market cap of roughly $1.13B, implying an unlock-to-market-cap ratio close to 14.6%. With only 28.32% of its maximum supply released, this event represents both a major liquidity injection and an early-stage tokenomics profile with substantial remaining locked supply, positioning H as a critical watch for June volatility.

HYPE – $39.04M unlock: HYPE is scheduled to unlock approximately $39.04M in tokens against a reported market cap of about $16.32B, keeping the unlock size well under 0.24% of market cap. With 43.52% of its maximum supply released, HYPE presents a mature emission curve where additional unlocks matter for trading dynamics but are unlikely to dominate price structure by themselves in the absence of other catalysts.

SAHARA – $34.69M unlock: SAHARA is set to unlock about $34.69M in tokens, against a reported market cap of roughly $115.22M, corresponding to an unlock near 30.1% of market value. Only 34.07% of its maximum supply is currently released, highlighting SAHARA as an early-emission infrastructure asset where vesting schedules will shape supply dynamics significantly.

HOME – $34.16M unlock: HOME’s upcoming unlock is around $34.16M, compared with a reported market cap near $173.27M, yielding an unlock of roughly 19.7% of market cap. With only 37.5% of supply released, HOME is in an early-curve phase where recurring unlocks remain a central part of the investment narrative and pose elevated dilution risk.

ZRO (LayerZero) – $29.31M unlock: ZRO’s unlock is approximately $29.31M versus a reported market cap of about $287.09M, implying a relative unlock size on the order of 10.2% of market cap. With 53.28% of maximum supply released, ZRO remains mid-curve, making the combination of substantial remaining supply and high relative unlock a notable factor for cross-chain infrastructure investors.

SPK – $21.15M unlock: SPK faces an unlock of approximately $21.15M against a market cap of $64.88M, representing roughly 32.6% of market capitalization. With only 32.52% of supply released, SPK presents one of the highest relative dilution risks in the top-tier category this month.

Mid-Tier Unlocks ($5M–$10M Range)

The mid-tier bucket includes tokens with unlocks in the $5M–$10M range that may be less headline-grabbing in absolute terms but still meaningful, especially for small- and mid-cap projects.

Key examples include:

- WET – $17.60M unlock, with 23% of supply released and a reported market cap around $15.82M, implying an extreme unlock-to-cap ratio exceeding 111%

- CONX – $16.47M unlock, with 89.92% released and a market cap near $30.61M, representing approximately 53.8% of market cap

- MEGA – $15.58M unlock, with only 7.47% released and a market cap around $70.84M, yielding a relative unlock size of about 22%

- ME – $14.55M unlock, with 50.61% released and a market cap near $47.40M, putting relative unlock size at roughly 30.7% of market cap

- SUI – $12.11M unlock, with 40.1% released and a market cap around $3.56B, representing a minimal 0.34% of market cap

- APT (Aptos) – $10.57M unlock, with 66.2% released and a reported market cap around $769.27M, yielding an unlock of approximately 1.4% of market cap

According to Tokenomist data, these mid-tier events often produce the sharpest local volatility, particularly where unlocks exceed 20% of market cap and liquidity is relatively thin.

Standard-Tier Unlocks ($2M–$5M Range)

Notable standard-tier unlocks include ARB ($9.45M), NEWT ($9.45M), MBG ($8.08M), KAITO ($8.08M), XPL ($7.83M), EIGEN ($7.75M), YZY ($6.32M), GPS ($5.40M), SOSO ($4.58M), BR ($4.55M), STRK ($4.90M), RED ($4.90M), OPN ($4.32M), KMNO ($4.26M), SEI ($3.74M), OP ($3.67M), ENA ($3.56M), LINEA ($3.37M), SOON ($3.27M), GUN ($2.78M), CHEEL ($2.80M), UDS ($2.54M), PEAQ ($2.54M), ZK ($2.50M), MOVE ($2.49M), ID ($2.45M), IO ($2.37M), LISTA ($2.29M), and ZETA ($2.19M).

Unlock Value Distribution

The distribution of unlock values suggests a three-tier structure consistent with monthly calendars:

High-value unlocks ($10M+): A small subset of tokens (H, HYPE, HOME, SAHARA, ZRO, SPK, WET, CONX, MEGA, ME, SUI, APT, ARB, NEWT, MBG, KAITO, XPL, EIGEN) account for the majority of the $580.33M total.

Standard unlocks ($500K–$10M): The bulk of tokens fall into this middle band, contributing moderate supply increments that can still be meaningful for individual price action but are unlikely to move the broader market on their own.

Micro unlocks (<$500K): A significant number of tokens including DCB, TRIBL, VRTX, NYAN, FORT, YALA, MMX, and dozens of others have small unlocks measured in tens of thousands of dollars or less. These typically have minimal effect outside of very illiquid markets or thinly traded pairs.

From a liquidity standpoint, traders should focus primarily on the high-value and high-ratio unlocks; the rest form background supply noise unless coinciding with strong narratives or extremely constrained floats.

High-Dilution Risk Tokens

Tokens with large unlocks relative to market cap and/or early-stage released percentages present the highest near-term dilution risk.

Notable high-risk profiles include:

- WET: $17.60M unlock vs $15.82M market cap (111%), with only 23% of supply released, marking an unprecedented dilution event that could trigger extreme volatility

- CONX: $16.47M unlock vs $30.61M market cap (53.8%), with 89.92% of supply already released, representing a large one-time liquidity event despite limited remaining future dilution

- SPK: $21.15M unlock vs $64.88M market cap (32.6%), with only 32.52% released, suggesting both steep current unlock and substantial future issuance

- ME: $14.55M unlock vs $47.40M market cap (30.7%), with 50.61% released, inviting elevated volatility around the event

- SAHARA: $34.69M unlock vs $115.22M market cap (30.1%), with 34.07% released, pointing to early-curve tokenomics with meaningful remaining emissions

- MEGA: $15.58M unlock vs $70.84M market cap (22%), with only 7.47% released, indicating one of the earliest-stage major unlocks this month

- HOME: $34.16M unlock vs $173.27M market cap (19.7%), with 37.5% released, another early-stage asset under steady supply expansion

- GUN: $2.78M unlock vs $17.72M market cap (15.7%), with 27.93% released

- H: $164.46M unlock vs $1.13B market cap (14.6%), with only 28.32% released, representing the largest absolute unlock with significant relative impact

These tokens are most vulnerable to post-unlock selling pressure if recipients are motivated to realize gains or rebalance positions, especially in environments of low demand or thin order books.

Sector-Level Observations

June 2026 unlocks span multiple crypto verticals:

- Infrastructure and base-layer ecosystems: H, HYPE, APT, ARB, SUI, SEI, STRK, ZK, IOTA, OP, LINEA, ZRO, SAHARA, EIGEN

- DeFi, staking, and financial primitives: IO, PEAQ, SOLV, FUN, AERO, KMNO, MAV, MANTA, REZ

- Gaming and metaverse-adjacent assets: PIXEL, YGG, VOXEL, ANIME, PRIME

- AI and specialized infrastructure: FET, AGIX, KAITO, AI, XPL

- Exchange or service tokens and miscellaneous utilities: CONX, CYBER, XCN, KAT, W, BMT, ME, and others

This breadth indicates that supply expansion is not isolated to one vertical; instead, unlocks touch multiple segments of the crypto stack during June, from core L1/L2 infrastructure to niche experimental tokens.

Market Impact Assessment

Price Pressure Considerations

Relative size: Unlocks exceeding 15% of market cap (for example, WET, CONX, SPK, ME, SAHARA, MEGA, HOME, GUN, H) are most likely to generate meaningful pressure, especially if liquidity is limited.

Emission stage: Early-curve tokens with low “Released %” (for example, MEGA at 7.47%, ACS at 10.75%, CYPR at 11.04%, H at 28.32%, STRK at 32.66%, ZK at 30.23%, SPK at 32.52%, SAHARA at 34.07%) remain structurally exposed to recurring dilution over extended periods.

Unlock structure: Although the unlock schedules do not clearly distinguish between daily linear releases and cliff-style distributions, large monthly unlocks often cluster around specific dates, increasing the risk of short-term intraday volatility.

For large-cap tokens like HYPE, SUI, APT, ARB, SEI, and FET, unlocks of under 2% of market cap are typically absorbed more efficiently. In HYPE’s case, the recent HYPE price rally demonstrates strong market demand and liquidity, which may help offset potential selling pressure associated with upcoming token unlocks.

Liquidity Absorption Capacity

The $580.33M monthly unlock value is moderate compared to quarterly figures that can exceed $1B+, suggesting that the broader market should have adequate capacity to absorb the aggregate supply under normal trading conditions. Similar to the June 1–7 token unlocks period, liquidity conditions and investor sentiment will play a critical role in determining how efficiently markets absorb newly released supply. However, liquidity is not evenly distributed: some tokens enjoy deep order books and multi-venue listings, while others trade on a limited set of exchanges with thin liquidity.

As a result, idiosyncratic volatility is most likely in:

- Small-caps with high relative unlocks (WET, SOLV, FUN, KAT, PEAQ, GUN, MEGA)

- Mid-caps with early-phase emissions and multi-million dollar unlocks (STRK, ZK, SAHARA, HOME, SPK, H, YZY)

Strategic Insights for Investors

Risk-Management Approaches

During months with concentrated unlocks, investors and traders closely following tokenomics vesting updates may consider:

Position sizing and leverage control: Avoid heavy leverage or oversized positions in tokens facing unlocks above 10–15% of market cap, particularly in thinly traded names.

Event-driven timing: For volatile unlocks, historical patterns often show post-unlock relief once the event passes and selling pressure is absorbed; traders may wait for this clearing period before adding exposure.

Diversification: Spread exposure across tokens with different emission profiles, emphasizing large-caps or late-stage tokens with high “Released %” when seeking reduced dilution risk.

Opportunity Identification

Unlock months can also create constructive entry points rather than just risk:

Mature tokenomics: Tokens with >70% released and moderate unlock sizes (for example, GAL at 89.83%, TRIBL at 94.23%, NTX at 97.2%, BIM at 88.63%, BMEX at 91.67%, YGG at 93.35%, DCB at 94.38%) often face limited future structural dilution once current events are priced in.

High-quality infrastructure names: For HYPE, APT, ARB, SEI, SUI, STRK, ZK, and IOTA, modest relative unlocks may simply represent periodic supply emissions in fundamentally important networks; temporary dips around unlocks can offer long-term accumulation opportunities.

Idiosyncratic dislocations: In smaller tokens, disproportionate price reactions following unlocks can sometimes overshoot fundamentals, creating contrarian trade setups for disciplined participants.

Tokens to Monitor Closely

Based on absolute unlock size, relative unlock-to-market-cap ratio, and supply-curve stage, the following tokens warrant particular attention in June 2026:

H Network: Largest unlock ($164.46M) with high relative size (14.6% of market cap) and only 28.32% released.

WET: Extreme unlock-to-cap ratio exceeding 111% ($17.60M vs $15.82M cap) at only 23% released, presenting the highest dilution risk of the month.

SAHARA, HOME, SPK: Multi-million dollar unlocks representing 19.7%–32.6% of market cap at relatively low released percentages (32.52%–37.5%), highlighting acute near-term overhang.

MEGA: $15.58M unlock at only 7.47% released (22% of market cap), indicating one of the earliest-stage major unlocks with substantial future dilution runway.

ZRO, STRK, ZK: Multi-million dollar unlocks in early-to-mid-stage infrastructure tokens (30.23%–53.28% released), where recurring emissions will remain central to valuation and positioning.

HYPE, APT, ARB, SUI, SEI: Large-cap names with meaningful absolute unlocks but modest relative dilution, important for broader market sentiment and narrative flow rather than acute supply shocks.

Conclusion

June 2026 presents a substantial but manageable token unlock window: $580.33M in scheduled releases across 144 projects, dominated by a concentrated cluster of high-value, high-ratio events in H, HYPE, SAHARA, HOME, ZRO, SPK, WET, CONX, MEGA, ME, and several others. For most of the market, these unlocks are digestible and unlikely to trigger systemic stress, but for individual tokens, especially those with unlocks exceeding 15–20% of market cap short-term price risk is elevated.

Investors navigating this period should balance defensive positioning in high-dilution names with opportunistic strategies in fundamentally strong projects where unlocks are already well telegraphed and modest relative to valuation. As tokenomics across the industry continue to mature, with many assets now past their most aggressive emission phases, months like June 2026 increasingly function as targeted, event-driven trading environments rather than broad structural shocks to the entire crypto market.

Reference: The complete dataset supporting the June 2026 Token Unlocks report is available for download on GitHub.

{kind=link}